Investment Basics: Inflation and Taxes

My first rule of investing is that a person shouldn’t invest in anything they don’t understand. If you can’t explain it, can you really know whether or not you’ve made a good decision? One day, we’ll each stand before God and give an account for our actions, including the way we’ve managed His resources. Can we claim that we were good stewards if we blindly invest in things we don’t understand? Some would argue that is not all that different from gambling since there is no wisdom behind the decision.

Poor decisions come in two forms. The first is the person that takes unnecessary risks with their investments, whether out of greed or ignorance, and puts the entire amount in danger of being lost. The other is the person that is so scared of risk that they don’t do anything and like the slothful servant in the Parable of the Talents in Matthew 25 squanders the opportunity to be a wise steward and earn at least a little interest on their savings.

My suggestion is for individuals to take financial education in small pieces, but commit to always be learning. This article is the first in a series describing various aspects of investing. My goal is to help you better understand the things you may already be doing and hopefully open your eyes to a few new concepts. As a more informed investor, you will be better equipped to steward the money God has given you to manage by avoiding dangers and capitalizing on good opportunities.

Today, we’re going to look at two silent dangers that eat away at our savings over time, inflation and taxes. They may seem harmless enough, but they can certainly do some damage.

Inflation

Simply defined, inflation is the decrease in what a dollar can buy over time due to an increase in costs. We’ve all experienced inflation in one way or another with the most common being the increased price of our groceries. Inflation has averaged about 3% per year over the last 80 years. That may not sound like much, but realize that with a 3% inflation rate, prices will double every 23.5 years. When it comes to investing, inflation is the silent killer for the person that sticks their money in a mattress or leaves it sitting in a bank account earning little or no interest. The thing to realize is that if you don’t earn more than the current rate of inflation, your money is going to be worth less in the future.

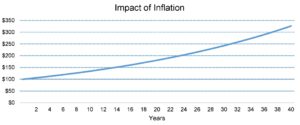

The following chart illustrates the impact of 3% inflation on the cost of living over a 40 year timeframe. In it we see that an item which costs $100 today will cost $181 in 20 years and $326 in 40 years.

A 3% average rate of inflation is pretty tame. If you look back at the early 1980s, we had inflation rates over 13% per year. Imagine how quickly your money was losing value in those years if you had it stored away in cash earning nothing. I often hear people reminiscing about the good old days when they could earn 10% or more on their bank CDs, but what they don’t think about is the high rate of inflation that was eroding that interest. They would have needed to earn a 13% return just to break even one of those years.

History provides us with some disastrous case studies of inflation from just the last 100 years. Germany suffered severe inflation in the years following WWI. From 1919 to 1923, prices skyrocketed. It is said that in that 4 year time period, a single loaf of bread went from costing 1 mark in 1919 to costing 100 billion marks by 1923. Prices were increasing so rapidly that workers would get paid several times in the same day so they could take their wages and buy things before the prices changed again. At its worst point, prices were doubling every 4 days.

While Germany is an extreme example, other countries such as Zimbabwe and Hungary suffered through even higher rates of inflation. All this brings to light the massive impact that inflation can have on the value of our money. Imagine being a retired person living on a fixed income during those years. What may have been a sufficient income at the beginning would have been worthless just a few years later.

Regardless of the real rate of inflation that we experience in our lifetimes, we need to be aware of the danger it poses and make sure we’re protecting ourselves against its eroding effects.

Taxes

Taxes are essentially fees charged by government entities to individuals or corporations that are then used to provide common services for the citizens and support for the operational activities of the government. Some common forms of tax are income tax, sales tax, property tax, etc. Regardless of the type of tax, the one thing they all have in common is that they decrease the overall value left for the consumer paying the tax.

As an investor, it’s important to understand the impact taxes have on our financial situation. When not sheltered from taxes, our investments may incur taxable gains in the form of interest, dividends or capital gains. In the case of these taxable earnings, an investor will need to use some of their gains to pay the taxes, leaving them with less than 100% of the increase earned by their investment.

When possible, we should seek out ways to be tax efficient by reducing the effect of taxes on our investment gains. We’re not looking to evade taxes that we rightfully owe, but instead, we want to understand and use the tax laws to our maximum advantage in order to grow our investments at a faster pace.

As an example of a tax saving plan, let’s look at a traditional 401k account offered through an employer. In this type of plan an individual is typically able to contribute money to a retirement account on a pre-tax basis. That means that any money contributed to the plan goes in before income taxes are withheld. This allows the investor to make a larger contribution to their account than if taxes had been taken out. In addition to avoiding income tax on the contributions, the investment earnings inside this retirement account (interest, dividends, capital gains, etc.) are not taxed as long as the money is not withdrawn from the retirement account. In other words, if you start saving for retirement at age 25 and leave the money in the plan until you’re age 65, you will pay no taxes on 40 years of investment gains until you start withdrawing the money from the plan during your retirement years. This deferred method of taxation allows your investments to compound at a more rapid pace than if they had been taxed along the way. If you know anything about compound interest, the benefit of 40 years of deferred taxes can have a huge impact on your account value.

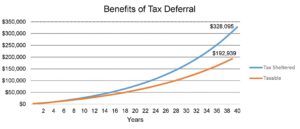

Following is a chart illustrating the impact of tax deferral using some random assumptions. The blue line represents an annual pre-tax contribution of $2,000 growing tax deferred at 6% a year. The gold line represents a taxable account receiving an annual after-tax contribution of $1,600 earning a net after-tax return of 4.8%. These numbers assume a 20% tax rate to be conservative. As you can see, the tax sheltered plan accumulates a much larger balance over the years. While taxes would be incurred on distributions taken from the tax-sheltered plan during retirement, it should still be the big winner.

It’s important to note there are other types of retirement plans available with different tax benefits and incentives. It’s beyond the scope of this article to explore all those options but it is a wise idea to consider using different tax strategies. It’s common knowledge that we should diversify our investments to reduce risk, but we can also hedge against future tax risks by using different types of plans.

Some will ask why the government provides these type of tax incentives. The simple answer is that the government is offering tax incentives because they want us to save for our retirement years. When we save, there’s less risk of the government needing to take care of us in retirement.

Conclusion

An investment education is important if we plan to steward God’s resources well. The goal for this knowledge isn’t to become the next Warren Buffet. Rather, we simply want to be informed individuals making wise decisions. Ignoring economic issues may sound like an appealing option to some, but a lack of knowledge can prove to be costly. Whether we avoid investing altogether and lose out to inflation or we invest in things we don’t understand, we risk being poor stewards of the resources we’ve been entrusted to manage.

Brad Graber, CFP® has been working with clients on personal financial planning and investment issues since 1996. He invests his time mentoring and educating individuals on ways to be better stewards of the resources God has entrusted to them.

***Disclaimer: The investment and tax information contained in this article is general in nature, is provided for informational purposes only, and should not be construed as investment or tax advice. I am not an accountant and cannot guarantee that such information is accurate, complete, or timely. Federal and state laws and regulations are complex and subject to change. You should consult an accountant regarding your personal tax situation.

Totally don’t understand inflation.

I have often thought their investments were things I trusted other people with. I have been challenged to consider this more thoughtfully. Thank you for the article.

Actually I pulled out of 401K’s after 2000 since the companies in which I had them kept changing investment companies, collecting with each transfer more in fees than I even contributed. So certain companies made a lot on my 401K, but for me it was basically flushing 7% of my income down a hole. Since then, my shyness to try again has probably cost something. I rolled what was left of my 401k’s into IRA’s, where I am not permitted to contribute, because I am eligible for 401K. Closing in on 65 years and working a in a very unstable business sector, I am not sure of the benefit of enrolling for 2019. I believe the company will match up to 1.5% after one is vested.